Last year marked a tentative conclusion to the COVID pandemic, which has prompted significant shifts in the economy over the past couple of years. These changes have reverberated across various sectors, including the veterinary practice market. Notably, the economy has grappled with pronounced fluctuations in interest rates, affecting the veterinary practice landscape and other industries. Over an 18-month span, interest rates escalated from zero to 5.25 percent,1 culminating in the containment of soaring inflation—a phenomenon reminiscent of the early 1980s. After peaking at nine percent in mid-2022, inflation subsided to a range of three to 3.5 percent by the end of 2023.2 The rise in interest rates has increased borrowing costs for buyers, and thus has negatively impacted business acquisitions and practice valuations for those hoping to sell to the corporate market.

Veterinary practice sales to corporate entities have undergone significant changes in the last two-and-a-half years. These shifts include everything, from pricing dynamics, deal structures, seller profiles, the likelihood of deal closure, and more. It is important to note this discussion is primarily concerned with corporate sales, as opposed to the doctor-to-doctor hospital sale market—comprising smaller practices with less than $1.5 million in revenue. The latter segment, which has its own distinct drivers, has exhibited more valuation stability compared to the corporate sale market.

Outlined below are the 10 most important shifts we have witnessed in the veterinary practice market in 2024, compared to 2021:

1) Visit volume

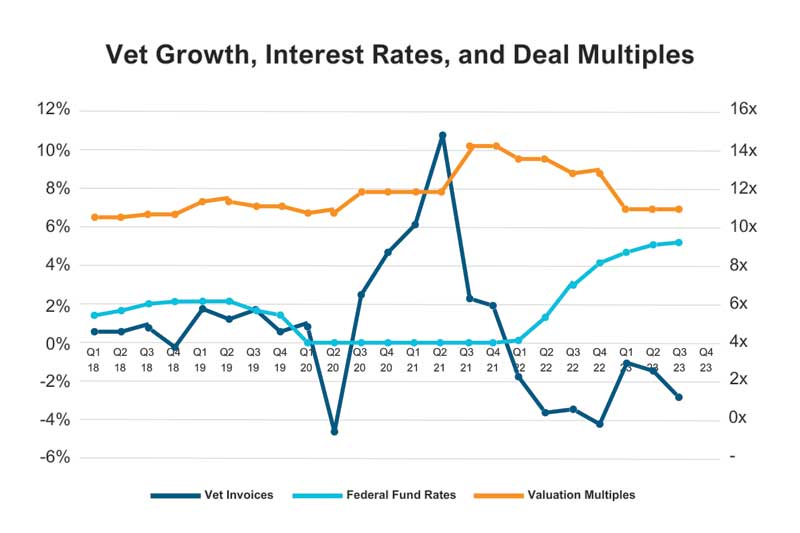

The year 2021 witnessed an unprecedented surge in demand, largely driven by pet adoptions amid the COVID pandemic among higher-income pet parents.3 This resulted in a six to seven percent increase in veterinary visits for the entire year, a dramatic increase from the stable but modest one percent growth seen during the preceding decade. This level of growth led to hopes that the demand growth might be sustainable over the long term. Yet, in 2022 and 2023, the industry “came back down to earth,” as visit growth receded by over three percent in 2022 and continued to decline by over two percent

in 2023.4

We project a return to the historical one percent visit growth trajectory in late 2024.

2) Valuation adjustment

The unprecedented valuation “bubble” that characterized veterinary hospitals and other industries in 2021—attributable to the pandemic’s demand surge coupled with the Federal Reserve’s retention of zero percent interest rates—has moderated in 2023. The rise of five percent interest rates and sluggish visit growth has grounded veterinary valuations from the 12 to 18x EBITDA (earnings before interest, taxes, depreciation and, amortization) highs of 2021 to a more realistic 8 to 12x EBITDA in 2023.5 Regardless, current pricing remains attractive relative to historical norms as it is similar to pre-COVID valuation levels observed in 2018 and 2019.

3) Structured transactions gain prevalence

Higher interest rates in 2023 prompted buyers to offer sellers less cash during closing, and instead opting for more deferred payments. Presently, 50 to 70 percent of the payment is in cash at closing, in contrast to 65 to 90 percent cash seen in 2021.5 Consequently, today’s deals have more “structure,” featuring seller notes, Top Company (TopCo) equity (ownership in the buyer), and joint ventures (retaining ownership in your hospital). This added structure is used to align incentives for both parties, and in particular, ensures the seller stays motivated to grow the business post-transaction.

4) The retirement mirage

Transactions today typically stipulated that owners who are major revenue generators, remain engaged for three to four years post-sale, working the same hours as before. When considering retirement, practice owners should decide how soon they want the option to slow down or retire. The earliest this option can typically happen is within the 3.5-year timeline (six months for the entire sale process, plus the three-year work requirement) for practices being sold to corporate buyers. Buyers now incorporate mechanisms or “hooks”—such as deferred payments or risks of TopCo (top company or parent company) equity loss—to ensure compliance with said employment agreements.5

Contrasting the frothy 2021 market, where work commitments sometimes spanned 12 to 18 months, today’s trend leans towards longer post-deal employment periods.5

5) Associate retention incentives

Given the ongoing recruitment challenges in the industry,6 associate retention incentives have gained traction in most, if not all, practice sales. These incentives take the form of gradual cash payments, minor ownership stakes in individual hospitals, and occasionally, TopCo equity in the buyer. The scale of incentives hinges on an associate veterinarian’s tenure and revenue contribution.5 For instance, an associate veterinarian, with 10 years at the practice and producing more than their pro rata share of revenue, will receive more substantial incentives than an associate with six months of tenure who contributes less revenue. While buyers may navigate the funding of incentives differently, the ultimate source remains consistent.5

What that essentially means is, whether a buyer offers a larger purchase price but has the seller fund the retention incentives, or the buyer offers a lower purchase price and the buyer funds the incentives, it all comes from the same pie.

6) Changing landscape of buyers

The “who’s who” of buyers has shifted drastically. In 2021, at least five consolidators purchased over 50 hospitals. Today, we expect at least three groups to have the same level of “aggressive” acquisition in the market.5 However, these groups are distinct from their 2021 counterparts–they are all different buyers. Recognizing the assertive buyers is pivotal in positioning a veterinary practice for sale. Simultaneously, there are several groups that were not as assertive and instead execute a consistent strategy of incremental growth, adding 10 to 30 clinics annually. 5

7) Heightened buyer due diligence

The post-letter of intent (LOI) diligence phase has evolved, now including more intensified information requests from buyers.5 Over the past two-and-a-half years, buyers have increased their degrees of diligence with prospective acquisitions. As a result, sellers need to be well-organized and equipped with essential documentation. Practice owners should be well-prepared with employee benefit plans, vendor contracts, leases, practice management reports, and comprehensive financial records, encompassing personal expense receipts. Today’s scrutiny far surpasses the diligence standards of 2021.

8) Increased ‘re-trading’ and deal withdrawals

In the aftermath of signing LOIs in 2021, changes to deal terms (“re-trading”) or walking away from deals were rare. Closure rates for LOIs surpassed 95 percent then. Presently, with a more cash-constrained market environment, 80 to 85 percent of deals close, albeit with higher instances of re-trading and buyers reconsidering deals entirely. 5

Why are deals re-traded or withdrawn? Key reasons include the loss of a pivotal doctor post-LOI or unanticipated fluctuations in revenue or profitability trajectories. Maintaining focus on business operations throughout the transaction process is paramount to ensuring successful closures.

9) Evolving deal quality

Deal quality is an ambiguous term often defined by the average profitability of hospitals acquired by a given buyer. In 2021, larger clinics generating over $1 million in profit or EBITDA were sold at unusually high multiples and with frequency.5 Younger practice owners were selling given the unusually high prices.

In today’s market, retirement is the primary driver behind owners continuing to sell due to the decline from the high prices being offered by buyers. Several high-profit practice owners are biding their time, monitoring the prospect of multiples returning to 2021 levels, or at least exceeding the current valuation range. However, the enduring rise of interest rates, potentially extending until mid to late 2024, may extend the waiting game for “better” deals.

In today’s market, we are starting to see some of the large hospitals deciding to sell, and because of their “scarcity,” the practices are attracting substantial buyer interest. In turn, those large hospital sellers receive strong pricing within the current market (albeit below 2021 levels).5

10) Frozen recapitalization market

Larger consolidators—those with more than 100 locations—have delayed potential sales or initial public offerings (IPOs) until interest rates decline and the loan market improves. Private equity firms and family offices, the entities that own the more than 35 veterinary consolidators, finance their purchases of individual hospitals with debt.

When a private equity firm sells their stake in a consolidator (also known as a recapitalization event), the buyer uses a lot of debt.7 Consequently, heightened interest rates—escalating from zero percent in 2021 to 5.25 percent in 2023—have driven up loan costs to 10 to 11 percent for buyers.5 This transformation has discernible impacts on their business valuations and has led all the larger consolidators to delay any sales or IPOs.

The evolving landscape of today’s veterinary practice market brought forth key takeaways for individual practice owners. Firstly, the economy, notably interest rates, significantly impact valuations for those practices selling to corporate buyers. Secondly, determining the ideal exit timing hinges the practice owner’s personal and professional goals, in addition to the market. Lastly, while peak pricing had waned in comparison to 2021, current valuations remain favorable in the context of the industry’s last two decades.

Rich Lester has over 14 years of experience in the veterinary industry helping veterinarians achieve financial success. He founded Veterinary Practice Partners (VPP), a group that exclusively co-own hospitals with local veterinarians. Lester is now a CEO at Ackerman Group.

References

- Tepper, Taylor. 2023. “Federal Funds Rate History 1990 to 2022.” Edited by Benjamin Curry. Forbes Advisor. May 3, 2023. https://www.forbes.com/advisor/investing/fed-funds-rate-history/.

- U.S. Bureau of Labor Statistics. 2009. “12-Month Percentage Change, Consumer Price Index, Selected Categories.” Bls.gov. 2009. https://www.bls.gov/charts/consumer-price-index/consumer-price-index-by-category-line-chart.htm.

- New York Times. 2020. “A Rare Economic Bright Spot in the U.S. Health System: The Vet’s Office,” August 12, 2020. https://www.nytimes.com/2020/08/10/upshot/pets-health-boom-coronavirus.html.

- “IDEXX Q3 2023 Earning Highlights.”

chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.idexx.com/files/earnings-snapshot-2023-q3.pdf - Ackerman Group proprietary data.

- “Tackling the Veterinary Professional Shortage.” 2022. Mars Veterinary Health. March 2, 2022. https://www.marsveterinary.com/tackling-the-veterinary-professional-shortage/.

- “Solving for Private Equity’s Inflation Conundrum.” 2023. Bain & Company. February 27, 2023. https://www.bain.com/insights/solving-for-private-equitys-inflation-conundrum-global-private-equity-report-2023/.